Image

Opinion | Iko Knyphausen | Updated June 11th, 2026

Eleanor and Harold had been married for fifty-three years when the neurologist diagnosed Harold with Alzheimer’s disease. Throughout their lives, they adhered to societal expectations: Harold worked for three decades as a mechanical engineer, paid taxes, and maintained their mortgage, while Eleanor raised three children before returning to work as a school administrator. Together, they contributed to Medicare and Social Security for nearly five decades, saved $420,000, and owned a modest suburban home. In the language of the American promise, they had consistently followed the prescribed path.

Within four years of Harold’s diagnosis, Eleanor consulted an elder law attorney who, with professional sensitivity, advised her to consider divorcing her husband of fifty years. This recommendation was not due to personal desire or marital failure, but rather because existing laws had rendered their marital fidelity a financial liability.

This narrative illustrates how the current system penalizes longevity, compels couples to legally dissolve marriages to preserve them in practice, and is further deteriorating in 2025 and 2026. It also highlights alternative policy choices made by other countries and considers potential lessons for the United States.

When a spouse in the United States requires nursing home or memory care, the financial structure of American eldercare often leads to significant financial hardship. Medicare, the federal program funded by working Americans, does not cover long-term custodial care. It provides coverage for short-term skilled nursing following hospitalization, typically for only a few weeks. However, once ongoing assistance with activities of daily living is required, Medicare coverage ceases. Medicaid, the program designed for low-income individuals, will cover long-term care, but eligibility requires individuals to first deplete their financial resources.

In most states, qualifying for Medicaid requires reducing countable assets to $2,000. The national median cost for a semi-private nursing home room is currently $315 per day, exceeding $114,000 annually.1

Under Medicaid regulations, the ‘community spouse’—the partner who remains at home—may retain approximately $162,660 (the 2026 federal limit) in addition to the primary residence. All other assets are typically allocated toward nursing home expenses. Consequently, a couple’s lifetime savings can be depleted within thirty-six months, despite decades of responsible financial planning.

At this juncture, elder law attorneys often introduce the concept of ‘medical divorce,’ a term that reflects the difficult choices imposed by current policy.

A Medicaid divorce is not a dissolution of love or commitment. It is a legal strategy. By divorcing, a couple can restructure asset ownership so that the healthy spouse retains more than Medicaid’s spousal protection rules would otherwise allow. The marital estate is divided; the ill spouse, now legally single, qualifies for Medicaid faster and with less financial destruction to the surviving partner. The couple may continue to see each other daily. The emotional marriage survives. Only the legal one is sacrificed to the paperwork requirements of a system that has made lifelong partnership a handicap.

The practice is real, documented, and routinely recommended by elder law attorneys in every state. When the rational response to government policy is to undo a fifty-year marriage on paper, the policy has failed. Not the couple.

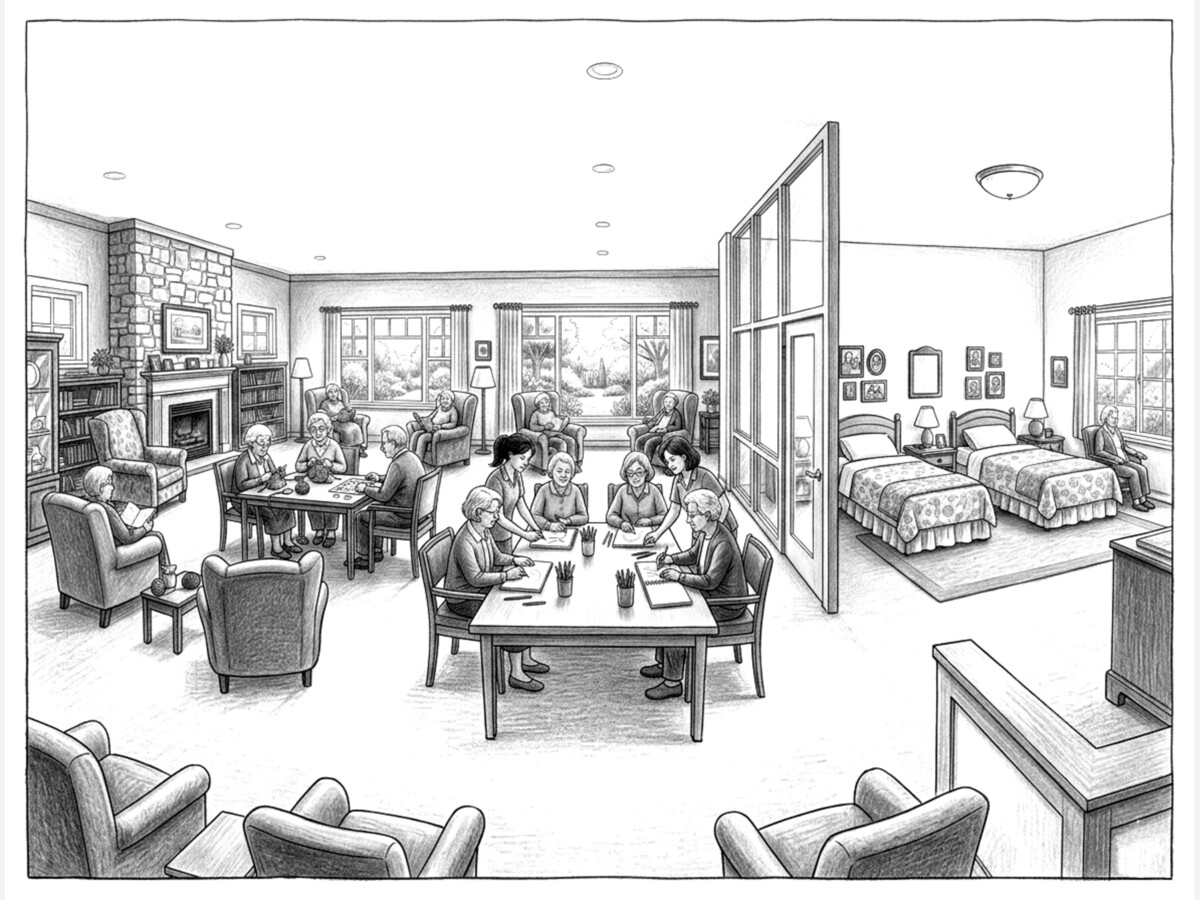

Alzheimer’s disease and related dementias make the financial catastrophe worse in almost every dimension. Nearly half of all nursing home residents have some form of dementia.2 Memory care is not simply assisted living; it requires secured environments to prevent wandering, staff trained in behavioral interventions, and higher staff-to-resident ratios, typically 15 to 25 percent more expensive than standard assisted living.3

A dedicated memory care community, the typical first placement for Alzheimer’s patients, runs a national median of $7,645 per month.4 As the disease progresses and medical needs intensify, most patients transfer to a skilled nursing facility at $9,000 to $10,600 per month.5 An average disease course of five to eight years can cost a family well over $1 million across both settings. The aggregate cost of memory care across the United States was projected at $781 billion in 2025, with an additional $247 billion in unpaid labor provided by family members.6 That last figure deserves a pause: a quarter of a trillion dollars in unpaid care annually, provided mostly by spouses and adult daughters, propping up a system the federal government has declined to fund adequately.

Americans are told, from their first paycheck, that they are investing in a social safety net. Medicare payroll taxes are withheld automatically: 1.45 percent from the employee and 1.45 percent from the employer, for every dollar earned, every year of a working life. Social Security takes another 6.2 percent from each side. For a middle-income couple working thirty to forty years, cumulative contributions easily reach $400,000 to $680,000 in nominal terms.7

The implicit bargain, reinforced by every political speech about “earned benefits,” is that in old age, when the body fails, and the mind dims, that system will be there. It is not there. Not for long-term care.

Medicare was never designed to cover custodial long-term care. This was a deliberate political choice made in 1965 and never revisited with the seriousness the demographic reality now demands. By 2030, all Baby Boomers will be 65 or older; by that point, one in five Americans will be at retirement age, according to Census Bureau projections.8 Roughly 70 percent of U.S. adults will need some form of long-term care in their lifetimes.9

The government’s recent policy moves compound rather than address the gap. In December 2025, the Centers for Medicare & Medicaid Services issued an Interim Final Rule rescinding the Biden administration’s 2024 minimum staffing standards for long-term care facilities. That rule was the first federal floor in American history for nursing care, requiring at least 3.48 hours of nursing care per resident per day and a registered nurse on-site around the clock. The stated reason was concern for rural and tribal facilities with workforce shortages; no replacement standard was offered.10 Seven months earlier, the One Big Beautiful Bill Act (signed July 4, 2025) cut nearly $930 billion from Medicaid over ten years. Medicaid funds care for approximately 62 percent of nursing home residents nationwide.11

The government simultaneously abandoned quality standards and cut the primary funding source. The people absorbing the consequences are elderly, often cognitively impaired, and unable to advocate loudly for themselves.

Compounding the staffing and funding crises is an ownership crisis most families never anticipate. Researchers estimate that private equity firms now own between 5 and 13 percent of American nursing homes. Most counts exceed 1,500 facilities, though opacity in ownership structures makes a precise figure difficult to establish.12 The PE playbook in long-term care is by now well-documented: acquire facilities, sell the underlying real estate to a separate trust, lease it back at rates that burden the operating entity with debt, cut staff to improve margins, and exit before the consequences fully materialize.

A 2025 AARP analysis of Florida nursing homes found that after private equity acquisition, the share of facilities rated one star by CMS (the lowest quality category) more than doubled, from 10 percent to 21 percent, while the share of five-star facilities halved, dropping from 28 percent to 14 percent. Direct care staffing fell 13 percent per resident, costing patients 33 fewer minutes of care per day.13 A peer-reviewed systematic review published in Health Policy in 2025, examining twelve studies from 2000 to 2024, found PE ownership consistently linked to higher rates of deficiencies, increased hospitalizations, and higher mortality.14

For context: 73 percent of American nursing homes are already for-profit. Private equity ownership represents the more extractive end of that spectrum, not a separate category.15

The natural question confronting a $10,000 monthly bill for a shared room and institutional meals is: why? You can rent an apartment for $1,000 a month. What accounts for the other $9,000?

The legitimate costs are real. A skilled nursing facility must maintain licensed nursing coverage around the clock: registered nurses, licensed practical nurses, and certified nursing assistants, regardless of how many residents are on a given floor that night. Add dietary staff, housekeeping, laundry, activities coordinators, social workers, and administrators, and labor typically consumes 60 to 70 percent of operating costs. Liability insurance in the long-term care sector is substantial. Regulatory compliance has a price. None of this is invented.

But labor costs and regulatory burden do not fully explain the number. The rest of the explanation is less flattering to the system.

Medicaid reimbursement rates, set by individual states, are, in most cases, below the actual cost of care. A facility may spend $280 a day to care for a Medicaid resident and receive $220 in reimbursement. The industry has spent decades arguing that this structural deficit is unsustainable, and on that narrow point, it is largely correct. What it states less often is how the gap gets closed: by charging private-pay patients $300 to $400 a day. The family writing the $10,000 monthly check is not simply paying for their loved one’s care. They are subsidizing, at a premium, the underfunded Medicaid beds down the hall.

This is the spend-down trap made visible. You pay full private-pay rates, often for years, until your savings are gone. At that point, you qualify for Medicaid, your reimbursement rate drops, and you become, in the facility’s ledger, a loss. The system is designed to extract maximum payment from families while they have resources, then absorb them at below-cost rates once they do not. It is not a market. It is a one-way valve.

Private equity ownership increases the extraction. When a firm acquires a facility and sells the real estate to a related trust, the operating entity must now pay rent to its own former self. That obligation, typically several hundred thousand dollars a month for a mid-sized facility, sits on top of every other operating cost and must be recovered somewhere. It stems from staffing ratios, dietary budgets, and maintenance schedules. The $10,000 monthly bill does not purchase more care when a meaningful fraction of it is used to service debt and property obligations engineered by the ownership structure.

The international comparison is instructive. Dutch nursing home care costs roughly $8,000 per month, with the government subsidizing residents to varying degrees; most families pay a fraction of that directly.16 Dutch wages are in fact lower than American ones in nominal terms, which accounts for some of the cost difference. But labor costs alone do not close the gap. American private-pay rates run $10,000 to $12,000 a month, not mainly because of those higher wages, but partly because a significant fraction of the bill is not care at all: it is the Medicaid cross-subsidy, the private equity rent extraction, and the administrative overhead of a fragmented multi-payer system. The Dutch deliver comparable quality at lower per-resident costs, even after accounting for the wage differential. Single-payer long-term care is cheaper in part because it does not incur the overhead of operating as a multi-payer system.

The $10,000 monthly bill is not the cost of care. It is the cost of care plus the cost of a broken financing system, plus the cost of profit extraction, plus the tab for decades of public underfunding. The family writing the check bears the full amount. The industry profits from most of it. And the government, which designed the conditions that make it possible, pays for none of it until the family is broke.

The United States spent 1.3 percent of GDP on long-term care in 2021. The OECD average was 1.8 percent. The Netherlands spent 4.4 percent.17 This is also the country that spends nearly twice the per-capita average of peer nations on total healthcare ($14,775 versus $7,860) and yet sits in the only major category in which it spends less than comparable countries per person: long-term care.18

The contrast with peer nations reveals political choice rather than fiscal necessity.

Germany introduced mandatory long-term care insurance (Pflegeversicherung) in 1995. Every working German pays into a dedicated fund, currently approximately 3.4 percent of gross income, split between employer and employee. Coverage is universal and not means-tested. There is no spend-down requirement analogous to Medicaid’s $2,000 asset floor. Families are not required to impoverish themselves to obtain care for a spouse. Germany spent 1.5 percent of GDP on long-term care in 2017, more than the U.S., and had universal coverage with no equivalent to medical divorce.19

Japan adopted a similar model in 2000. Japan’s Long-Term Care Insurance covers all residents over 65, financed through payroll contributions and general tax revenue. Independent comparative health policy assessments rate it as generous by world standards.20 Only 7.7 percent of long-term care costs fall to individuals out of pocket; compulsory premiums and public funding cover the remainder. In the United States, the majority of long-term care costs ultimately fall to individuals and families.21

The Netherlands provides the most comprehensive coverage in the OECD: over 90 percent of costs covered publicly, no means-testing for institutional care, built on the principle that aging is a social risk to be shared collectively, not a private liability to be managed individually.22

The argument that the United States cannot afford such a system collapses when held against its own spending data. The money is not absent. The political will is.

The objections to a publicly funded long-term care system deserve acknowledgment. Critics point to fiscal sustainability: any American program now would serve an immediate, large aging population, involving considerable premiums or general revenue from the outset. The failure of the CLASS Act, a voluntary national LTC insurance program included in the Affordable Care Act and abandoned by the Obama administration in 2011 (formally repealed in 2012 after being deemed actuarially unsound), is frequently cited as evidence that the federal government cannot design such a program competently.23 Moral hazard concerns also emerge: if long-term care is publicly funded, will people underinvest in their own planning?

These are legitimate challenges, not dismissible objections. But they point toward program design, not program impossibility. The CLASS Act failed because it was voluntary, meaning only higher-risk individuals enrolled, and it suffered from the adverse selection death spiral that afflicts all voluntary insurance. The private long-term care insurance market has experienced the same failure: over 100 insurers offered LTC policies in 2000; fewer than a dozen remain today, having severely mispriced claims risk and dramatically raised premiums.24 Both failures confirm the same thing: long-term care is not insurable on a voluntary basis. It requires mandatory participation to pool risk across the full population, exactly the design that Germany, Japan, and the Netherlands have effectively implemented.

Washington State’s WA Cares Fund, which began collecting a 0.58 percent payroll tax in July 2023, is the first American proof-of-concept at scale: a mandatory public fund providing a lifetime benefit of up to $36,500 for qualifying care needs, beginning July 2026.25 The benefit is modest ($36,500 covers roughly three to four months of nursing home care at current rates), but the mechanism is real, the participation is broad, and the administrative infrastructure now exists. A ballot initiative to make participation optional failed in November 2024. It is a floor, not a ceiling, and it demonstrates that a mandatory payroll-funded approach is politically achievable at the state level.

The way forward does not require wholesale invention. The architecture already exists in three functioning models from peer democracies, a cautionary case study in what not to repeat (the CLASS Act), and a live American pilot (WA Cares). The essential features of a workable system are well understood: mandatory participation, payroll financing with progressive adjustments, universal eligibility regardless of assets, and benefits structured around assessed care needs rather than financial ruin.

A federal program modeled on Germany’s would, in rough order of magnitude, cost an additional 0.5 to 1.0 percentage point of GDP, achievable through a dedicated payroll contribution of approximately 1 to 2 percent. That is less than the annual premium increase many families already absorb on their private health insurance. It would eliminate the Medicaid spend-down trap, make medical divorce unnecessary, provide a funding floor for nursing home quality, and bring the United States into alignment with what the rest of the developed world considers a basic feature of civilized governance.

A near-term concrete step: Congress should commission a bipartisan long-term care financing study with an explicit mandate to model a mandatory public insurance program alongside incremental Medicaid reforms and to report within 18 months. Washington State’s WA Cares experience should be formally evaluated as a federal design template.

Eleanor did not think, when she married Harold in 1971, that the terms of their marriage included a clause requiring her to divorce him in order to survive his death. She should not have had to. The attorney’s advice was not cruel; it was correct. The cruelty belongs to the system that made it necessary.

America has spent sixty years building a healthcare apparatus of extraordinary technical sophistication, consuming a larger share of national income than any other country, and has chosen not to cover the one category of care that virtually every older American will eventually need. Germany decided otherwise in 1995. Japan in 2000. Washington State in 2019.

The question is not whether a different system is possible. It plainly is. The question is whether the country will decide, before the full demographic wave breaks, that the people who built it are worth caring for.

Notes & Sources

Opinion June 2026

Sunny, with a high of 80 and low of 54 degrees. Sunny during the morning, clear overnight.

YES! Very well said and well researched. Thank you.

After I completed the very first Community Police Academy (I would highly recommend participating in this), I had the honor of doing my "ride along" with Sgt Walker. A true compassionate professional and an asset to our LFP police department.

What an excellent choice. Chief Zanella will do an excellent job leading our LFP PD.